Why Christmas 2018 maybe wasn’t so bad for retail after all

Christmas season 2018 trading performance. Note: Selfridges covers first 24 days of December only

Despite reports of plunging consumer confidence, Brexit “jitters” and “the worst November on the high street ever” (according to the Anti-Claus, Sports Direct owner Mike Ashley), Christmas trading doesn’t seem to have turned out as badly as expected. There have been no profit warnings (so far), one disastrous performance (Mothercare) and a couple of poor ones (Sainsbury’s and Topps Tiles – the latter against strong 2017 comparatives). On the other hand, Dunelm, Ted Baker, Selfridges and Greggs have impressed with their strength and Majestic Wine, Aldi, Morrisons and Next have been respectable. While there are some major retailers left who could potentially bring down the batting average (Debenhams, Tesco, Asda and M&S), overall consumer Armageddon seems to have been put on hold. So why is this?

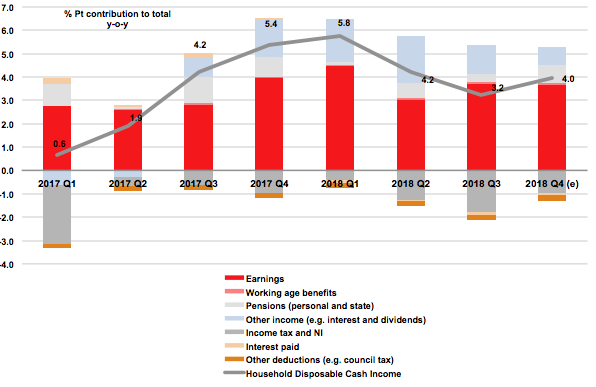

1) Household net income (above) is growing reasonably strongly. Spring 2018 saw a rapid increase, which it now appears was even stronger than originally estimated, and autumn saw a renewed improvement, helped by a buoyant jobs market and rising wages;

2) Consumers are still increasing their borrowing, including credit cards, and, more importantly, have yet to be spooked into saving more;

3) Consumer confidence, although lower than it was, is not actually low by historical standards, despite what a whole raft of retailers and commentators may say about it;

4) Inflation is falling, helped in particular in December by cuts in petrol prices.

Looking forward into 2019, the best that can be said is that households enter the new year with finances strengthening, and this should provide some momentum for the first quarter, helped by weak comparatives from 2018 trading, affected by the Beast from the East. The main recommendation is to ignore reports of “low” consumer confidence and focus on real world indicators of prices, jobs and wages. If these remain stable and positive, then we can be reasonably confident of rising retail sales. On the other hand, if they go haywire in the coming months, then it is time to take cover.